Key benefits

- Comprehensive offering: Euribor complements Eurex’s Euro government bond futures, OTC IRS swaps clearing and Repo offering.

- Margin Efficiency: Eurex Clearing’s Prisma margin methodology offers Cross-margining opportunities with Euro LTIR Futures as well as Euro OTC Swaps cleared at Eurex Clearing. Click here for more information about Prisma.

- Liquidity: Order book liquidity supported by dedicated market makers enabling anonymous trading in the CLOB.

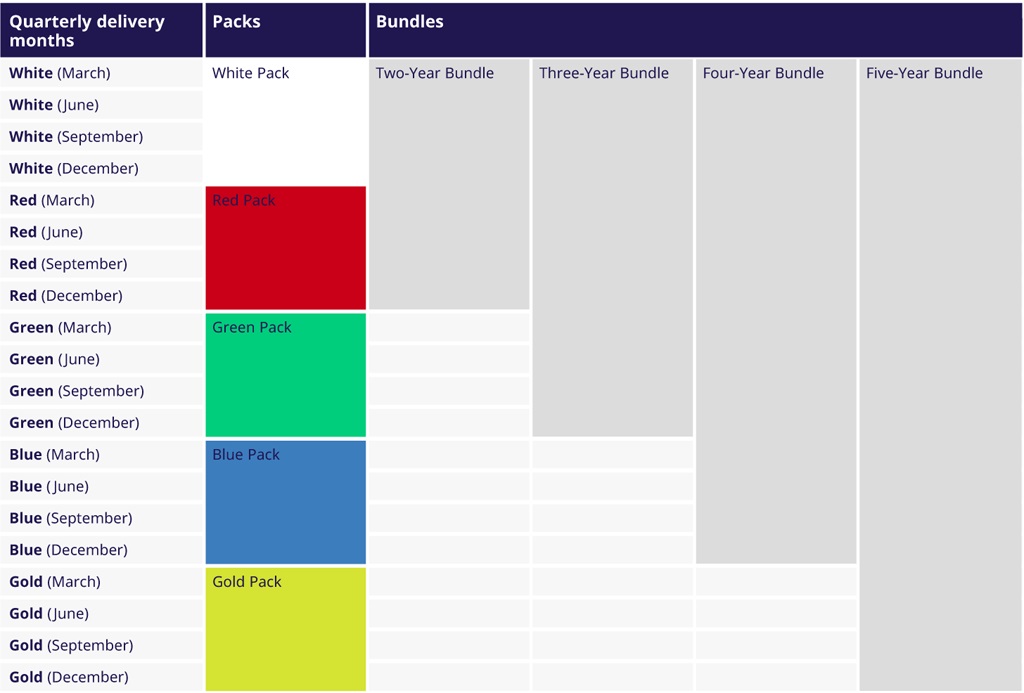

- Flexibility: Can be traded in the order book or via TES (Block). Packs & Bundles offer an efficient way to hedge longer exposures at a reduced cost. Inter-product spreads offer efficient execution of a strip of Euribor futures against a Euro-Schatz future.

Prices FEU3

| Product | Diff. to prev. day last | Last price | Contracts | Time |

|---|---|---|---|---|

| FEU3 | +0.01% | 97.505 | 1 | 17:27:46 |

Packs and Bundles strategies